Intersecting Disruptions: The Hidden Inflection of AI-Driven Data Centre Crypto Integration and Structural Credit Dynamics

As AI advances reshape banking and finance, an underappreciated inflection is emerging at the nexus of AI, data centres, cryptocurrency market regulation, and structural credit markets. This intersection may compel a fundamental reshuffling of capital allocation norms, regulatory frameworks, and industrial architecture over the next two decades.

This paper identifies a weak signal suggesting that the integration of advanced AI workloads with crypto-native data centres paired with nascent regulatory shifts (such as South Korea’s limits on crypto equity exposure) can catalyse new systemic feedback loops. These loops could alter financial infrastructure dependencies, credit risk underpinnings, and industrial concentration in unforeseen ways.

Signal Identification

The development qualifies as a weak signal—technically nascent, unevenly visible, but plausibly transformative within a 10–20 year horizon. This signal is grounded in the emerging convergence of:

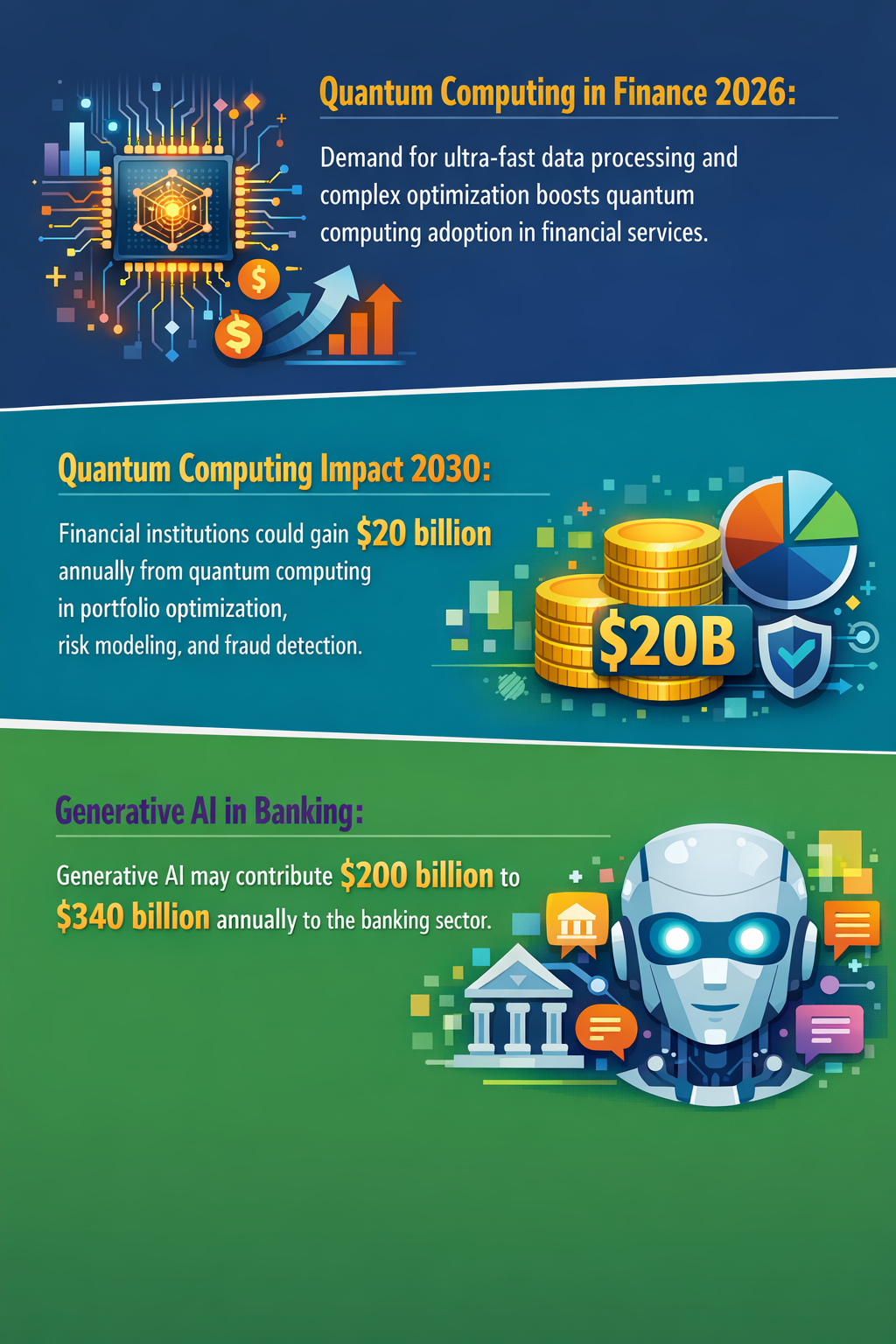

- Generative AI’s soaring computational and banking sector impact (with estimated value creation of up to $340 billion annually in financial services)

- Crypto regulatory frameworks beginning to embed exposure caps into corporate capital structures (e.g., South Korea’s 5% equity investment ceiling in digital assets)

- Rapid data centre specialization to support both AI workloads and crypto proof-of-stake or other consensus validation, effectively merging computational infrastructure footprints

- Structural credit market fragilities tied to evolving digital asset risks and open banking innovation with multi-trillion-pound economic potential

This intersection is not yet widely recognised as a coherent systemic inflection, despite discrete coverage of each component (>50% plausibility given current trajectories). Impact sectors include financial services, industrial data centres, regulated banking, and capital markets infrastructure.

What Is Changing

Multiple reports document powerful value addition from generative AI in banking, estimating $200–$340 billion in sector-wide annual gains (AlphaBold 16/03/2026; Architech Today 01/02/2026). This computational surge demands increasingly specialized data centres engineered to accommodate AI’s intensive requirements, including enhanced energy efficiency and processing capacity.

Concurrently, South Korea’s Financial Services Commission is pioneering guidelines restricting public companies to allocate no more than 5% of equity capital into leading digital assets (Bitcoin Foundation 07/04/2026). This regulation presages a broader institutionalisation of crypto-related credit risk management embedded within balance sheets.

Meanwhile, open banking adoption is projected to generate upwards of £43bn annually for the UK economy through platform-enabled financial service innovation (FinTech Global 12/03/2026). This paradigm collapses traditional credit and payment boundaries, fostering increased transparency but also new operational and systemic risk contours.

What is under-recognised is how these developments intersect robustly via data centre infrastructure. Emerging crypto-native data centres, essential to supporting blockchain validation (e.g., proof-of-stake mechanisms) and AI model training, are gradually converging functionally. This integration creates a structural duality: computational hubs simultaneously underwriting AI banking applications and crypto market validations.

This duality may intensify systemic risk transmission from crypto asset volatility into credit markets more acutely than anticipated, especially given evolving regulatory thresholds and increasing reliance on AI for credit underwriting and risk modelling. This creates a feedback loop between technological infrastructure concentration, capital markets, and regulatory oversight frameworks.

Disruption Pathway

The maturation of high-density AI and crypto workloads sharing data centre ecosystems may accelerate the formation of specialised industrial clusters. Conditions accelerating this include falling costs of renewable energy (facilitating sustainable compute), further regulatory attempts to cap crypto exposure, and institutional adoption of AI-enhanced credit analytics.

As financial institutions increase AI dependency for transaction processing, pricing, and credit risk assessment, their exposure to the combinatorial hazards of crypto asset volatility and data centre operational disruptions may grow. This introduces stresses on credit markets, where digital asset-backed securities or credit derivatives become more commonplace but also entwined with new infrastructure dependencies.

In response, banks and regulators could pivot toward integrated supervision models encompassing computational infrastructure resilience, cryptographic asset market risks, and AI governance frameworks. This may prompt structural adaptation—such as new capital adequacy metrics accounting for infrastructure concentration risk, or licensing regimes for data centres performing dual critical functions.

A second-order effect might be industrial consolidation driven by firms controlling both AI-optimised and crypto-validation data resources, potentially reshaping supplier-buyer power balances in technology procurement and financial service intermediation.

Such cross-domain feedback loops could unintentionally amplify systemic fragilities, especially if regulatory arbitrage or blind spots emerge between AI model oversight and crypto asset market surveillance. Hence, dominant banking and industrial regulatory paradigms may evolve from siloed entity supervision to hybrid infrastructure-market co-regulation.

Why This Matters

For capital allocators, this signal highlights the need to reassess exposure to crypto assets embedded indirectly through data infrastructure and AI-enabled credit instruments. Regulatory bodies may need to preemptively expand frameworks to address multi-domain systemic risks, rather than treating AI, crypto, or banking sector issues as isolated.

Competitors who secure footholds in convergent data centre ecosystems might capture outsized advantages in capital-efficient AI computations and stable crypto market servicing. Supply chains for data centre equipment and energy procurement could realign around geographical hubs benefiting from this dual demand.

This intersection also shifts liability paradigms, where failures in AI decision-making or crypto validation processes compound credit defaults, raising complex challenges in governance and operational risk management.

Implications

This emerging inflection could plausibly reshape industrial architectures by 2035 or earlier. It may catalyse novel regulatory models fusing technological infrastructure oversight with financial supervision. The signal should not be dismissed as mere crypto hype or incremental AI progress; instead, it reflects system-level coupling effects currently underappreciated.

Competing interpretations might view these trends as manageable technological specialization without systemic consequence. However, given the scale projections for AI-driven banking impacts and increasing mandation of crypto asset exposure caps, this convergence merits strategic foresight.

Capital flows may increasingly favour integrated platform providers who can manage cross-domain risk, incentivising mergers or new consortium models. This could weaken traditional monoline data centre operators and unregulated crypto networks.

Early Indicators to Monitor

- New capital expenditure announcements for data centres explicitly targeting joint AI and blockchain/crypto workloads

- Patent filings related to integrated AI-crypto data processing and risk assessment technologies

- Venture capital clustering on startups blending AI credit analytics with crypto market infrastructure

- Regulatory consultations expanding crypto exposure limits or imposing dual-function data centre requirements

- Corporate capital allocation disclosures referencing AI-crypto asset synergies or capping digital asset investments

Disconfirming Signals

- Persistent divergence or specialization of AI and crypto data centre infrastructure without convergence

- Significant regulatory relaxations removing crypto exposure caps in major markets

- Lack of institutional adoption of AI-augmented credit instruments linked to crypto markets

- Major data centre failures not impacting interconnected credit or crypto market dynamics

- Technological stagnation in AI or crypto consensus methods limiting cross-sector synergies

Strategic Questions

- How can financial regulators integrate oversight across computational infrastructure, crypto asset markets, and AI-driven credit models to mitigate emerging systemic risks?

- Should capital allocation strategies prioritize investments in dual-service data centres and integrated fintech infrastructure platforms anticipated to dominate 2030 banking ecosystems?

Keywords

Generative AI; Crypto Regulation; Data Centres; Structural Credit Risk; Open Banking; Financial Services Commission; Capital Allocation; Systemic Risk

Bibliography

- Generative AI could add between $200 billion and $340 billion in value annually to the banking sector. AlphaBold. Published 16/03/2026.

- Generative AI could add between EUR 190.84 billion and EUR 324.43 billion annually to the global banking sector. Architech Today. Published 01/02/2026.

- The Financial Services Commission has been weighing guidelines - ones that could let qualified public companies put no more than 5% of their equity capital into leading digital assets. / South Korea. Bitcoin Foundation. Published 07/04/2026.

- Open Banking could generate as much as £43bn in annual value for the UK economy as adoption expands across financial services. FinTech Global. Published 12/03/2026.