Analysis of recent evidence in the domain of Electrolysis highlights several key patterns gaining momentum linked to technological advancements, policy frameworks, market growth, and strategic energy transitions. Signals cluster into themes around green hydrogen scale-up, electrolyzer technology development, renewable integration with electrolysis, and geopolitical shifts impacting energy security. These dynamics collectively indicate a systemic transformation driver for clean energy systems with accelerating opportunities for green hydrogen production and deployment.

| Signal Name / Theme | Direction | Relative Momentum | Short Commentary |

|---|---|---|---|

| Green Hydrogen Electrolysis Capacity Expansion | Accelerating | 5x increase in low-emission H2 production projects planned by 2030; electrolyzer capacity from 1 GW to 20 GW (2023-2026) | Substantial policy support and investment globally for electrolyzer gigafactories and scaling green hydrogen production underpin rapid market growth and technology deployment. |

| Water Electrolysis Machine Market Growth and Tech Evolution | Accelerating | CAGR ~14.6% projected 2026-2036; shift from pilot MW scale to multi-gigawatt commercial projects; focus on cost reduction from $500-$1,200/kW down to $200-$300/kW | Manufacturing scale-up, technology innovation in alkaline, PEM, and SOEC systems, plus tightening cost structures are driving rapid industrialization of electrolyzers. |

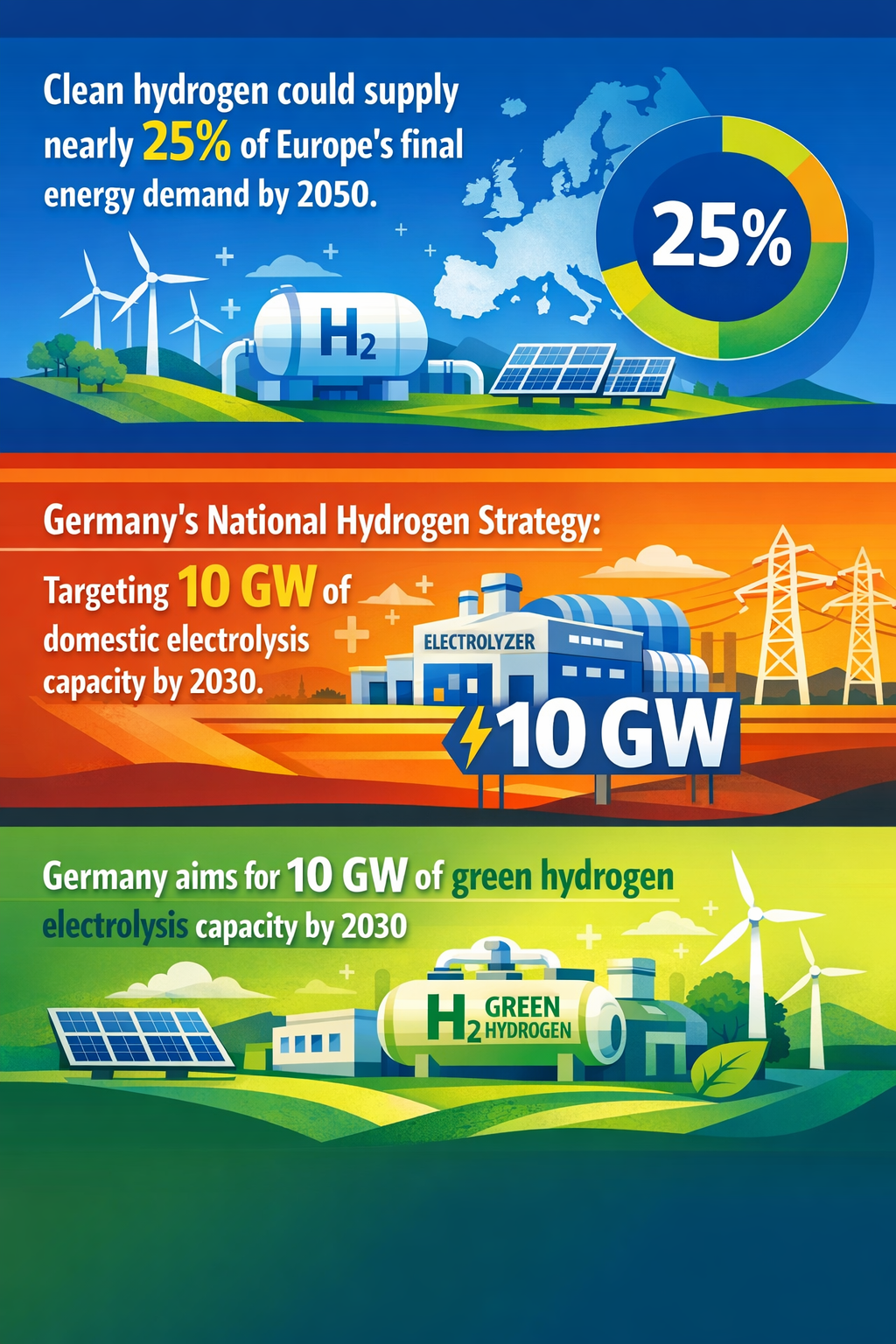

| Integration of Electrolysis with Renewable Energy and Energy Security | Accelerating | EU scenarios show up to 50% reduction in natural gas use by 2050 via renewables and green hydrogen; increasing coupling of wind/solar with electrolysis and energy system transition plans | Multi-sector decarbonization strategies leverage electrolysis combined with renewable capacity expansion to enhance energy independence and climate mitigation. |

| Advanced Electrolysis Technologies (SOEC) and Industrial Demo Projects | Accelerating | Commissioning of world’s largest SOEC electrolyzer (Dutch refinery, 2026); pilot projects integrating hydrogen into refining and industrial processes | High-temperature electrolysis demonstrations highlight efficiency gains and industrial applicability, driving confidence and scaling of emerging electrolyzer tech beyond PEM and alkaline. |

| Policy and Regulatory Support for Electrolysis and Hydrogen | Accelerating | Multiple governments with hydrogen strategies (60+ globally); funding programs like EU Hydrogen Bank, U.S. Inflation Reduction Act incentives; new carbon pricing and hydrogen certification schemes | Robust policy frameworks and financial incentives lower market barriers and mobilize private investment, fostering demand creation and technology diffusion for electrolysis-based hydrogen. |

The electrolysis domain is witnessing convergent trends where technological innovation, market scale-up, and policy momentum reinforce one another. There is a clear trajectory from pilot and niche electrolyzer deployments towards gigawatt-scale manufacturing and widespread industrial applications, driven by steep cost reductions and heightened demand for green hydrogen as a flexible decarbonization vector. The integration of electrolyzers with accelerated renewable energy capacity targets within regions like the EU underscores a strategic transition focused on reducing fossil fuel dependency and enhancing energy security. Additionally, emerging SOEC technology demonstrations in industrial settings indicate a diversification of electrolysis solutions optimized for higher efficiencies and specialized applications.

Policy instruments play a critical role in setting a stable market environment and enabling investments for scaling electrolyzer production, hydrogen infrastructure, and end-use demand creation—especially in harder-to-electrify sectors such as heavy industry and long-haul transport. Regional growth heterogeneity is notable, with Europe, North America, and Asia Pacific as leaders but emerging markets like Mexico gaining significant traction due to resource endowments and proximity to key buyers. The collective acceleration of these signals forebodes a period of rapid technology maturity and commercial deployment, vital to meeting mid-century climate objectives.