Our Scans

·

Insurance Pricing

·

Rumsfeldian Logic

1. Known Knowns

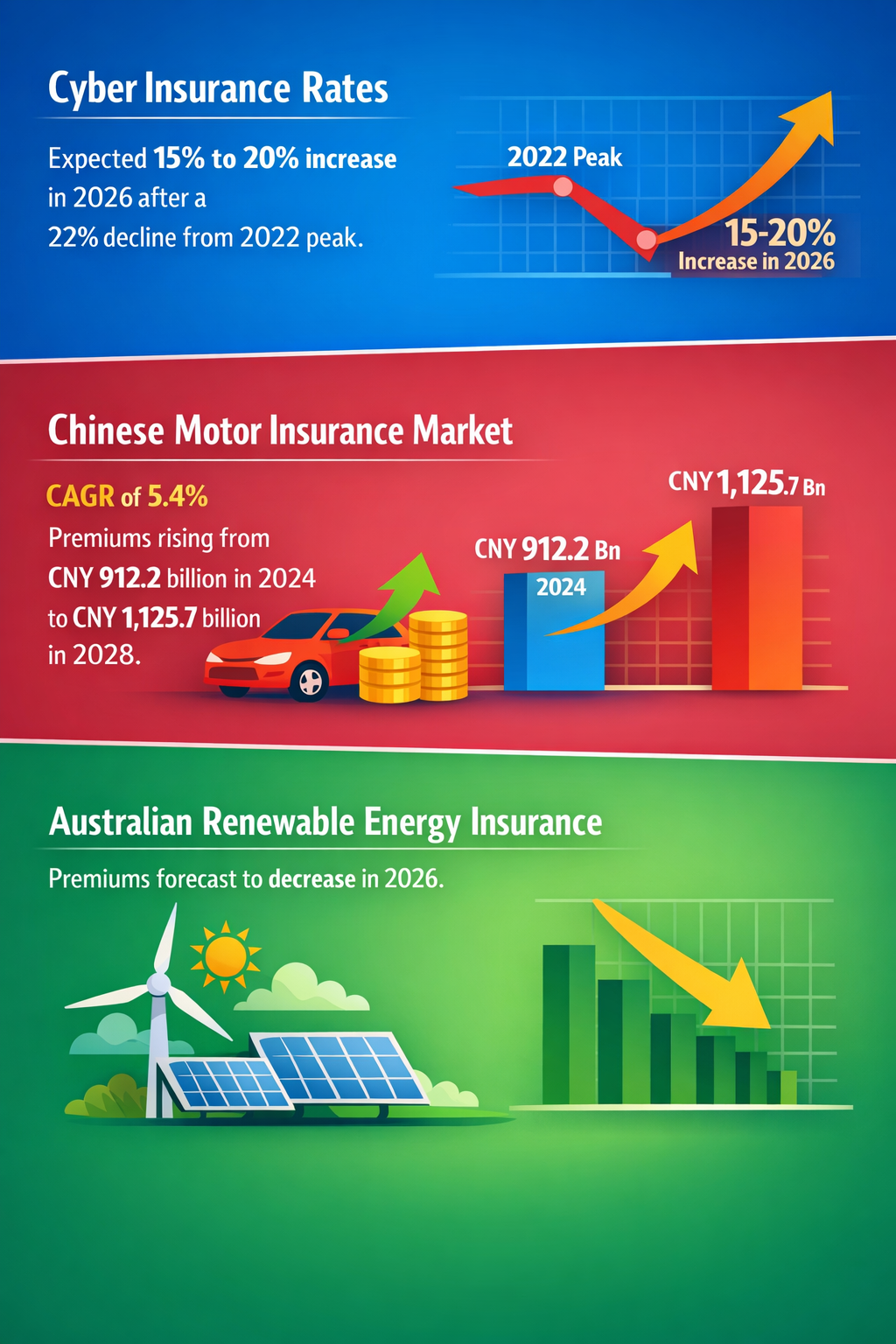

- Global cyber insurance premiums are stabilizing after rapid growth, with projected increase to $16.4 billion in 2026 and a 15-20% rise in cyber insurance rates following a recent softening (Swif.ai).

- Ransomware remains the dominant driver of large cyber claims by value (60%), though faster detection and technical controls have halved claim severity recently.

- Insurance pricing for home and commercial lines is headed upward, driven by more frequent and severe natural disasters, with home insurance rates rising 4% on average in the U.S. in 2026 (ProgramBusiness) and commercial lines seeing moderated but continued increases (Business Insurance).

- Renewable energy insurance premiums in Australia are forecast to decline in 2026 due to maturing technology and better operational data, despite risks from extreme weather (IndexBox).

- Taiwan’s insurance market is expanding with strong growth in motor and property lines, supported by demographic and risk factors, showing the importance of local context in pricing (Insurance Business).

2. Known Unknowns

- The medium-term impact of AI-driven cyber threats on loss severity and pricing remains uncertain, with early signs influencing underwriting but full risk modeling still evolving.

- How rising weather-related catastrophe frequency will affect insurance pricing volatility and availability, especially in heavily exposed regions, is not fully predictable.

- The trajectory of small and mid-sized business (SMB) cyber insurance uptake and claims experience is uncertain, with high exposure but uneven coverage and varying risk management maturity.

- Long-term operational and technological risk trends within emerging sectors like battery storage remain unclear due to limited historical claims data.

3. Unknown Knowns

- Insurers likely hold extensive internal data on preventative technology efficacy (MFA, EDR) that could be better leveraged to refine risk segmentation and pricing models.

- There may be underutilized insights around regional climate patterns and catastrophe modeling that can improve dynamic pricing and portfolio risk management.

- Existing knowledge within cyber underwriting teams about the cost-benefit of incident response retainers and backup strategies could inform product development and client advisory more aggressively.

4. Unknown Unknowns

- Emerging geopolitical cyber risks, particularly linked to state-backed attacks and evolving attribution protocols, could lead to unexpected claims denials and coverage gaps.

- Rapid technological breakthroughs or failures in renewable energy systems, AI security tools, or new insured assets may disrupt risk assumptions and loss trends.

- Systemic risks arising from interdependencies in cloud services and supply chains could cause correlated large-scale losses currently underappreciated.

5. Implications

- Short-term: Atradius should anticipate rising cyber and property rates, especially for clients lacking robust technical controls or operating in high-risk geographies.

- Medium-term: Increasing underwriting selectivity and tightened coverage terms may pressure SMB clients and sectors with emerging but uneven risk profiles (e.g., battery storage, renewables).

- Long-term: Adaptive risk assessment models incorporating AI threat evolution, climate change, and geopolitical complexities will be critical for sustaining competitive pricing and market share.

- Failure to incorporate evolving risk controls and data insights risks increased claim denials and reputational damage.

6. Recommendations

- Enhance data integration from internal underwriting and external sources to improve dynamic risk pricing, focusing on technical control efficacy and emerging risk signals.

- Develop product offerings and advisory services tailored for SMBs and renewable energy sectors, incorporating education on incident response and preventive controls.

- Invest in scenario planning and stress testing for systemic and geopolitical cyber risks, updating war exclusion language and claims handling protocols.

- Monitor regulatory changes and technological innovations closely to anticipate shifts in claims frequency/severity and pricing strategy adjustments.

Briefing Created: 10/06/2026