Decentralized, Edge-Integrated AI Infrastructure: A Weak Signal Poised to Reshape Industry Structure and Regulation

As AI adoption races toward ubiquity, an under-recognized shift toward decentralized, edge-based AI ecosystems is emerging. This weak signal indicates a future where data centers, regional interconnectivity, and AI processing embedded in billions of distributed devices redefine capital flows, regulatory boundaries, and competitive dynamics over the next two decades.

Conventional discourse has focused on hyperscale cloud AI infrastructure and concentration of compute power in global mega-cloud centers. However, developments in low-latency connectivity hubs, hybrid AI-cloud-edge computing models, and the explosion of AI-enabled end devices (from wearables to connected vehicles) suggest a structural inflection. The growth trajectory from centralized AI inference to distributed, edge-augmented intelligence has significant implications for industrial strategy, system resilience, and governance frameworks.

Signal Identification

This development qualifies as a weak signal with a medium plausibility band projected over a 10–20 year horizon, reflecting disruptive potential though presently underappreciated in mainstream strategic dialogues. It spans sectors including digital infrastructure, telecommunications, manufacturing, automotive, cybersecurity, and regulatory domains. Unlike the broadly acknowledged AI hype cycle around generative AI and hyperscale cloud investment, this signal is subtler — pertaining to the embedding of AI workloads increasingly at the edge facilitated by new low-latency connectivity and hybrid cloud configurations (DCTC GCC Blog 01/07/2026; AZoM 12/07/2026).

What Is Changing

The PwC survey highlights rapid scaling of AI, automation, and advanced technologies in manufacturing, forecasting tech enablement to more than double by 2030. Yet underpinning this is growing recognition that AI inference workloads are expected to dominate by 2027, increasingly executed closer to data sources to reduce latency and bandwidth demand (PwC 04/06/2026; DCTC GCC Blog 01/07/2026).

Crucially, the GCC (Gulf Cooperation Council) region’s investment focus on low-latency connectivity to Europe, Asia, and Africa underscores the strategic value of proximity in global AI data flows, hinting at a geographical decentralization trend balancing against traditional Silicon Valley and Taiwanese chip manufacturing dominance (DCTC GCC Blog 01/07/2026; Crypto Briefing 18/04/2026).

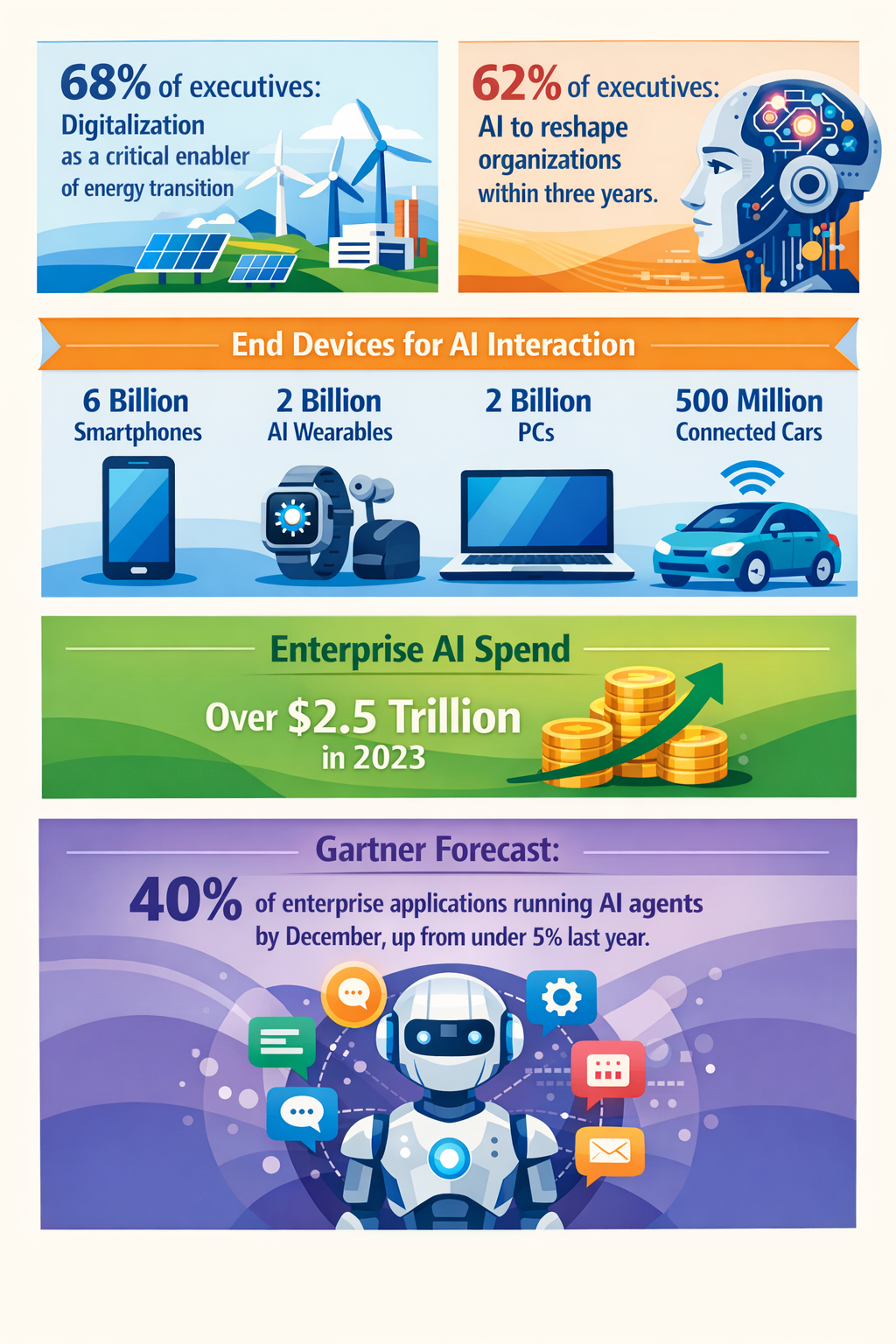

Simultaneously, the proliferation of AI-capable end devices—estimated at about 6 billion smartphones, 2 billion AI wearables, 2 billion PCs, and 500 million connected cars—positions vehicles and consumer electronics as critical AI gateways (Digitimes 21/03/2026). This shifts AI deployment from cloud-dominated to hybrid, distributed models requiring new infrastructural and governance approaches.

Moreover, as enterprise AI adoption quickens with nearly 40% of applications embedding task-specific AI agents by end-2026, operational execution increasingly depends on the integration of edge AI with cloud pipelines, introducing complex challenges in data sovereignty, security, and compliance (TechNova Partners 15/07/2026; EasyComm 28/06/2026).

Lastly, regulatory forces like the EU Cyber Resilience Act (EU CRA), mandating coordinated vulnerability disclosure and cybersecurity in IoT devices, imply formal recognition of the risks introduced by pervasive distributed AI systems (Cavli Wireless 09/05/2026). Together, these themes reveal a substantive shift toward a structurally hybridized AI infrastructure, blending cloud, edge, and device-level intelligence.

Disruption Pathway

This shift could escalate as the geometric growth of AI-enabled devices stresses centralized data centers’ bandwidth and latency limits, creating economic inefficiencies and performance bottlenecks. Operators may accelerate investments in regional data hubs, edge computing nodes, and specialized AI inference hardware closer to end users to optimize costs and user experience (DCTC GCC Blog 01/07/2026).

As these deployments scale, cybersecurity vulnerabilities multiply along distributed attack surfaces, prompting stricter regulatory frameworks and industry standards on data integrity, model validation, and real-time monitoring. Platforms like the Open Secure AI Alliance aim to remediate exposure by leveraging open-source security protocols — signaling early structural governance adaptations (CNBC 27/07/2026).

Simultaneously, new industry relationships and supply chain dependencies may form around regional hubs, challenging Asia-Pacific and Silicon Valley dominance. Hyperscalers may lose monopolistic control over AI workloads as edge providers and emerging economies with strategic connectivity advantages compete (Crypto Briefing 18/04/2026; PwC 04/06/2026).

Indeed, the combined effect of data sovereignty laws, latency-sensitive applications (e.g., automotive AI), and divergent regional cybersecurity regimes could fracture existing cloud-centric governance models, fostering a multipolar AI infrastructure ecosystem with distinct regulatory regimes adapting to local realities.

Why This Matters

For capital allocators, the emergent edge AI infrastructure will likely redirect billions in investment toward regional data centers, low-latency fiber optics, edge computing platforms, and semiconductor design specialized for distributed inference processing. Anticipating this transformation could capture value in new industrial segments while mitigating risks of stranded assets in oversized centralized AI infrastructure (Crypto Briefing 18/04/2026; CityAM 12/07/2026).

Regulators will face pressure to adapt frameworks for AI safety, data protection, and cross-jurisdictional enforcement amid distributed architectures. The EU Cyber Resilience Act’s mandates for IoT device security prefigure stronger governance on edge AI’s cyber risks, potentially influencing global standards (Cavli Wireless 09/05/2026).

Industrial strategists should note that decentralized inference capabilities embedded in vehicles and wearables will reshuffle market incumbencies. Dominant cloud providers might lose exclusivity as OEMs and telecom operators seize roles in AI delivery chains, compelling alliances and ecosystem shifts (Digitimes 21/03/2026).

Moreover, supply chains for AI chips need recalibration for the growing preference of inference-optimized silicon over training-oriented chipsets, generating new sourcing and manufacturing pressures (Crypto Briefing 18/04/2026).

Implications

The integration of distributed AI infrastructure may structurally reshape capital allocation by decentralizing compute investment and diversifying regional development priorities. This shift could provoke emergent regulatory ecosystems tailored to unique data sovereignty, latency demands, and cybersecurity risks rather than one-size-fits-all cloud regulation.

It might elevate regional players and new entrants who control or monetize low-latency connectivity, edge data centers, and AI-enabled consumer devices, thereby fragmenting the industrial structure that currently favours hyperscale cloud giants and chip foundries in East Asia.

This is not merely incremental scaling of existing infrastructure but represents a fundamental reconfiguration of where and how AI workloads are processed and governed, with systemic implications for security, liability, and operational continuity.

Alternate interpretations might argue centralized cloud infrastructure will remain dominant due to cost efficiencies and management simplicity. However, the combined technical, regulatory, and commercial pressures favor a more hybrid, multipolar ecosystem.

Early Indicators to Monitor

- Growth patterns in regional data center investments emphasizing edge compute (e.g., GCC, Europe), coupled with fiber-optic network expansions supporting low-latency connections.

- Regulatory developments following the EU Cyber Resilience Act on AI and IoT security compliance and coordinated vulnerability disclosure adoption.

- Procurement shifts by automotive manufacturers and OEMs toward embedded AI and edge inference platforms in vehicles and wearables.

- Venture funding clustering around startups developing hybrid edge-cloud AI software frameworks, inference-optimized chipsets, and cybersecurity solutions for distributed AI.

- Standards formation initiatives like the Open Secure AI Alliance addressing AI security vulnerabilities across distributed environments.

Disconfirming Signals

- Significant plateau or recession in edge infrastructure investment, especially if hyperscalers double down predominantly on centralized cloud AI.

- Failure of latency-sensitive AI applications to commercialize at scale, maintaining preference for centralized compute models.

- Lack of regulatory coherence or delays in cybersecurity standards for AI-enabled IoT and edge devices, resulting in stalled governance adaptation.

- Emergence of unresolvable technical barriers limiting efficient hybrid cloud-edge AI model integration and orchestration.

- Supply chain consolidation reinforcing monopoly control over AI chip manufacturing, undermining diversification to edge-optimized silicon.

Strategic Questions

- How should capital allocation strategies balance investments between centralized hyperscale AI infrastructure and emerging edge and regional compute assets?

- What regulatory frameworks and governance models are necessary to manage distributed AI’s cybersecurity, data sovereignty, and liability risks effectively?

Keywords

AI infrastructure; Edge computing; Low-latency networks; Distributed AI; Data sovereignty; EU Cyber Resilience Act; IoT security; AI chips; Hybrid cloud; Smart vehicles

Bibliography

- PwC's survey of global manufacturing leaders shows AI, automation, and advanced technologies moving rapidly from experimentation to scale. PwC. Published 04/06/2026.

- As AI inference workloads become dominant in 2027, the GCC’s low-latency connectivity to Europe, Asia, and Africa will become increasingly valuable. DCTC GCC Blog. Published 01/07/2026.

- If AI spending plateaus, TSMC could find itself with expensive excess capacity. Crypto Briefing. Published 18/04/2026.

- 40% of enterprise applications will incorporate AI agents for specific tasks by the end of 2026, compared with fewer than 5% in 2025. TechNova Partners. Published 15/07/2026.

- The EU Cyber Resilience Act (EU CRA) mandates implementing a Coordinated Vulnerability Disclosure (CVD) policy to enhance cybersecurity within the European Union, particularly for products such as IoT devices. Cavli Wireless. Published 09/05/2026.