Climate Adaptation Innovation as a Structural Economic Inflection for the UK

Emerging climate adaptation capabilities represent a subtle yet potent economic inflection that could reshape the UK’s industrial landscape, regulatory paradigms, and capital flows over the next two decades.

While much focus remains fixed on inflation volatility and commodity price shocks, the UK’s growing strategic emphasis on climate adaptation technologies and capabilities signals a disruptive pivot beyond mere mitigation efforts. This weakly recognised development suggests potential structural shifts in how capital is allocated, sectors evolve, and governance frameworks adapt, particularly through export-driven innovation and climate-resilience infrastructure. The interplay of rising private sector digital transformation, frontier technology investment, and evolving climate adaptation policies underpins an economic inflection point with far-reaching consequences.

Signal Identification

This development qualifies primarily as an emerging inflection indicator with medium to high plausibility over a 10–20 year horizon, impacting sectors including infrastructure, finance, technology, and government policy. Unlike incremental climate mitigation efforts, climate adaptation capability—entailing technological, institutional, and economic innovation to adjust to environmental impacts—has not yet fully penetrated mainstream economic foresight or capital deployment decision-making.

Its medium to high plausibility stems from strong governmental and institutional frameworks identifying climate adaptation as a critical growth lever, linked to export potential, yet its transformational impact is still nascent. The sectors most exposed include climate-tech manufacturing, AI-enabled infrastructure management, regulatory compliance industries, and financial services integrating climate risk into governance and capital allocation.

What Is Changing

The UK’s economic landscape is witnessing a convergence of several underappreciated dynamics grounded in the intersection of climate adaptation and frontier technologies. Official analysis highlights opportunities for the UK to deploy its specific capabilities toward climate adaptation to yield export growth and domestic resilience, marking a departure from conventional climate economics focused primarily on emissions reduction (UK Government 01/07/2026).

Simultaneously, rising private investment into AI infrastructure and digital transformation creates an enabling environment for sophisticated climate adaptation technology development and deployment (Spherical Insights 20/07/2026). This stands in contrast to conventional expectations that such innovation would be primarily carbon-mitigation oriented. Instead, frontier technologies are increasingly looking at adaptive capabilities such as predictive climate risk modelling, smart resource allocation, and resilient supply chain automation.

Meanwhile, persistent economic pressures such as inflation volatility from energy supply shocks and cost-of-living challenges underscore the urgent practical need for adaptation-focused economic strategies that increase systemic resilience rather than vulnerability (CPA UK 15/07/2026; The Guardian 28/07/2026).

This composite scenario signals a fundamental structural theme: the economic value of climate adaptation innovations as strategic capital allocation targets, export growth drivers, and risk governance instruments is emerging but not widely perceived. Unlike headline concerns around inflation rates or commodity price volatility (The Guardian 30/07/2026), this inflection carries systemic implications for industrial reconfiguration and regulatory frameworks.

Disruption Pathway

The climate adaptation inflection could evolve into structural change through a layered escalation. Firstly, increasing unpredictability in climate-induced weather and supply chain disruptions—amplified by volatile energy prices—will create growing economic incentives to invest in adaptive technologies and infrastructure. This may accelerate private and public capital shifting from traditional mitigation to adaptive solutions, driven by system stress and strategic foresight.

Such investment patterns will impose new stresses on existing regulatory models, which today primarily focus on emissions controls rather than adaptive capacity or resilience metrics. Governments and regulators would be compelled to develop and mandate new frameworks that incentivise climate resilience, potentially redefining industrial compliance standards, infrastructure build norms, and financial risk disclosures.

The industrial structure may adapt through the rise of “climate adaptation clusters,” integrating advanced AI, sensor networks, and resilient material technologies, which could redefine regional economic hubs within the UK. These clusters might spur export-driven growth by developing proprietary adaptation solutions fit for diverse global markets facing similar climate challenges.

Crucially, feedback loops may emerge where enhanced climate adaptation capabilities reduce economic volatility risks, fostering investor confidence and lowering the cost of capital for adaptive industries. Conversely, failure to advance adaptation may amplify systemic vulnerabilities, triggering regulatory reprisals and capital flight.

Under these dynamics, dominant economic and governance models anchored in conventional industrial policy and financial risk management could shift toward integration of climate adaptation metrics, creating new governance architectures combining technology standards, climate science, and economic foresight.

Why This Matters

Decision-makers overseeing capital deployment and industrial strategy would see significant exposure to this signal. Capital might need reallocation from short-term inflation hedging or mitigation-only climate investments toward adaptation innovation ecosystems.

Regulatory frameworks could be overhauled to incorporate climate adaptation standards, requiring anticipatory engagement to shape feasible policies and avoid disruptive compliance shocks. Competitive positioning requires this forward lens: firms investing early in adaptive technologies might secure dominant market shares in emergent global value chains.

Supply chains exposed to climate risk stand to be redesigned using adaptive technology, potentially altering procurement and liability models. Governance bodies will need new integrative capabilities to assess adaptation risks systematically across sectors, reducing misallocation and reinforcing resilience.

Implications

This inflection indicator might ultimately represent a new strategic axis for the UK’s economy that transcends transient economic noise such as short-term inflation changes or commodity price spikes. Climate adaptation innovation could transform capital allocation preferences and regulatory systems over 10–20 years.

It is not merely a niche sustainability add-on or a secondary policy concern but could evolve into a primary economic growth and risk governance driver. However, this interpretation competes with views that see adaptation as an incremental or purely technical effort, subordinate to aggressive decarbonisation.

The progression from weak signal to structural change is contingent on sustained private and public commitment, regulatory innovation, and technological breakthroughs that harmonise climate resilience with economic returns.

Early Indicators to Monitor

- Increased venture capital and private equity funding clustering in climate adaptation startups and technologies.

- Government and regulatory drafts that embed climate adaptation metrics into industrial, infrastructure, and financial compliance standards.

- Rising patent filings for adaptation-related AI controls, resilient materials, and infrastructure technologies.

- Procurement shifts favoring climate resilience infrastructure and adaptive technology deployment in public and private sectors.

- Formation of cross-sector adaptation innovation clusters and export partnerships targeting climate-affected economies.

Disconfirming Signals

- Major policy retrenchment or lack of regulatory innovation on climate adaptation standards.

- Failure of adaptation technologies to achieve cost competitiveness or scalability.

- Privatization or capital market focus constrained to carbon emissions mitigation exclusively.

- Stabilisation of energy prices and reduced climate-related economic shocks diminishing urgency.

- Significant backlash or political opposition limiting government support for adaptation investment.

Strategic Questions

- How can capital allocation strategies be adjusted now to anticipate the growing economic significance of climate adaptation innovation?

- What regulatory frameworks must be developed or updated to integrate climate adaptation metrics into governance across industries?

Keywords

Climate adaptation; Frontier technologies; Capital allocation; Economic inflection; Regulatory innovation; AI infrastructure; Climate resilience

Bibliography

- Economic opportunities of climate adaptation for the UK. UK Government. Published 01/07/2026.

- UK bets big on frontier technologies to lead global digital economy. Spherical Insights. Published 20/07/2026.

- UK business news today: Economy, markets, insolvencies. CPA UK. Published 15/07/2026.

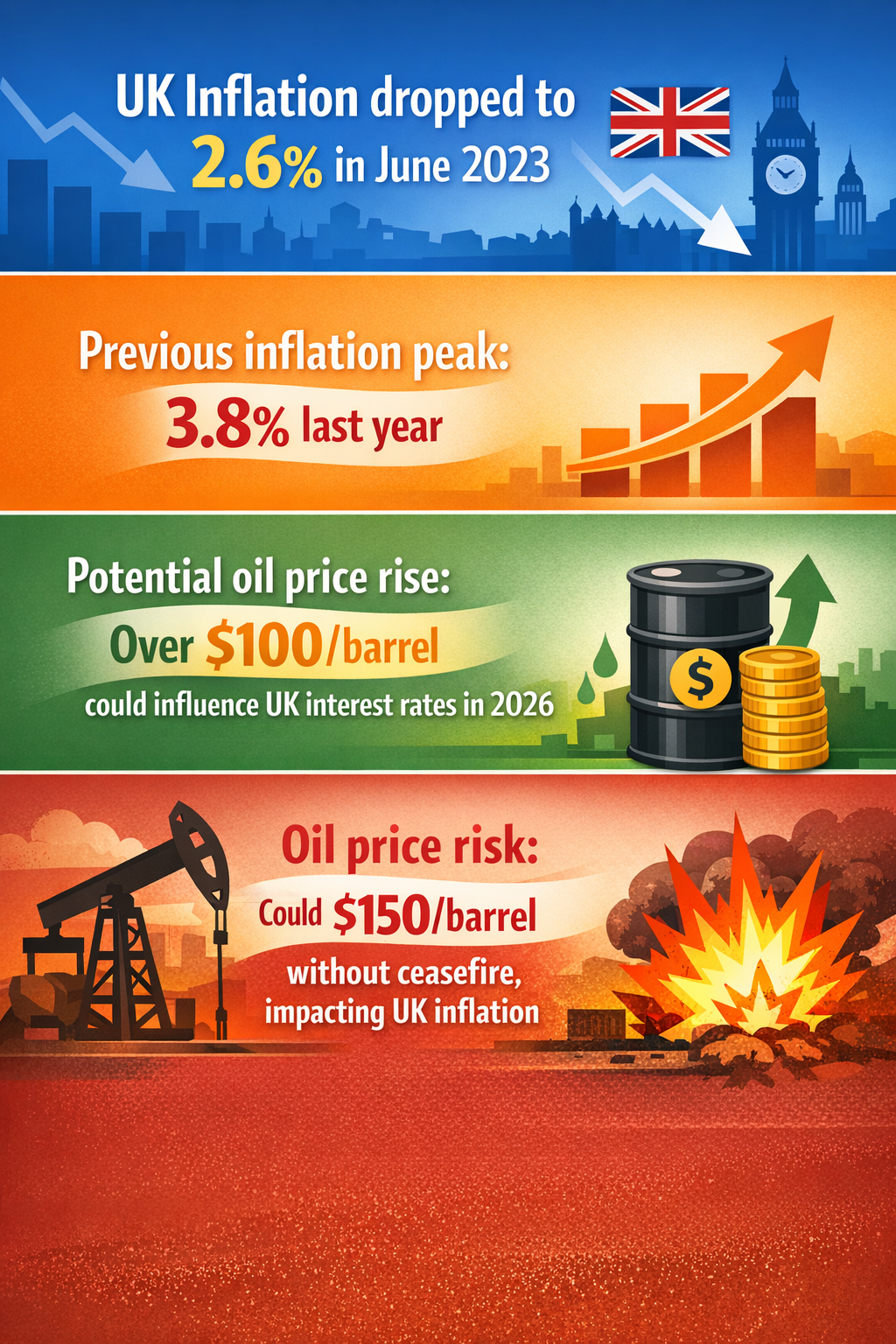

- UK inflation dropped by more than expected in June to 2.6%, but City economists are warning that the Bank of England could be forced to tear up its economic forecasts and raise interest rates later in 2026 if oil prices return to above $100 a barrel. The Guardian. Published 28/07/2026.

- Inflation in the UK fell by more than expected in June to 2.6%, down from a peak of 3.8% last year. The Guardian. Published 30/07/2026.